Your auto insurance premium just increased again. You open the renewal notice, see the new amount, and wonder if there's anything you can actually do about it.

Good news: there is.

Many Texas drivers assume they're stuck with whatever rate their insurance company assigns them. But the truth is, small adjustments to your coverage and driving habits can lead to significant savings. You don't need to sacrifice protection to pay less.

At Winkler Insurance Agency in Temple, TX, we've helped countless drivers find affordable auto insurance without cutting corners on coverage. These five strategies are simple to implement and can make a real difference in what you pay each month.

1. Bundle Your Policies for Multi-Policy Discounts

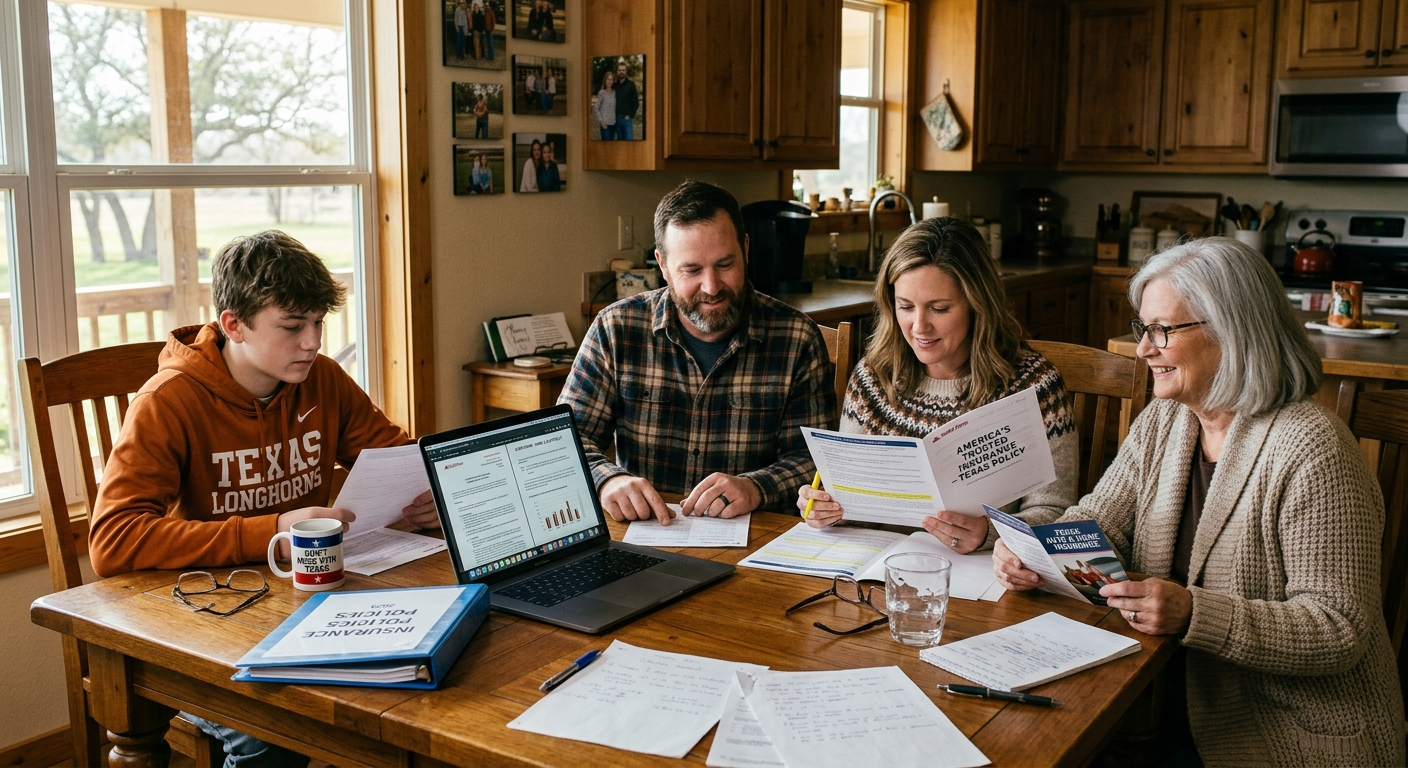

The easiest way to lower your auto insurance premium is to bundle it with your homeowners or renters insurance.

Multi-policy discounts

typically save you 15-25% on your auto insurance premium. Insurance companies reward customer loyalty, and managing multiple policies with one carrier is more efficient for them. They pass those savings on to you.

Here's how bundling works in practice:

- You purchase auto and home insurance from the same company

- The discount applies to both policies (though usually more to the auto policy)

- You get one renewal date and often one bill

- Claims and service become simpler with one point of contact

A Temple couple recently bundled their auto and home insurance and saved $840 annually. They didn't change their coverage amounts at all—just consolidated their policies.

When considering bundling, make sure the combined cost with discounts is actually lower than keeping policies separate. At Winkler Insurance Agency, we compare rates across multiple carriers to ensure bundling truly saves you money.

2. Increase Your Deductibles Strategically

Your deductible

is the amount you pay out of pocket before insurance kicks in when you file a claim. Raising your deductibles can substantially lower your premium.

Understanding the Deductible Trade-Off

Common deductible amounts range from $250 to $2,000. Here's the relationship:

Higher deductible = Lower premium

Lower deductible = Higher premium

Increasing your comprehensive and collision deductibles from $500 to $1,000 could reduce your premium by 20-30%.

Is a Higher Deductible Right for You?

Before raising your deductible, ask yourself:

- Do you have enough savings to cover the higher deductible if you need to file a claim?

- How often do you typically file claims?

- What's your risk tolerance?

If you have an emergency fund and you're a safe driver who rarely files claims, a higher deductible makes financial sense. You'll save money every month on premiums, and you'll still be protected against major losses.

For Texas drivers on tighter budgets, a moderate deductible ($500-$750) often provides the best balance between affordable premiums and manageable out-of-pocket costs.

3. Take Advantage of Available Discounts

Auto insurance companies offer dozens of discounts, but they don't always advertise them clearly. You have to ask.

Common Auto Insurance Discounts

Good driver discount:

If you've been accident-free and ticket-free for three to five years, you qualify for significant savings.

Defensive driving course:

Completing an approved defensive driving course in Texas can earn you a discount (and remove points from your license). The course takes just a few hours and savings typically last three years.

Good student discount:

Students under 25 with a B average or better often receive 10-25% off their premiums.

Low mileage discount:

If you drive fewer than 7,500-10,000 miles per year, you may qualify for reduced rates. With more people working from home, this discount has become more accessible.

Vehicle safety features:

Cars equipped with anti-lock brakes, airbags, anti-theft devices, and electronic stability control often qualify for discounts.

Paid-in-full discount:

Paying your six-month or annual premium upfront instead of monthly can save you 5-10%.

Paperless and automatic payment discounts:

These small discounts (usually $5-$20 per year) add up over time.

Discounts Stack

The power of discounts comes from combining them. A safe driver who bundles policies, drives a safe vehicle, and pays in full could save 40% or more compared to someone with no discounts.

Make sure your agent knows about life changes that could qualify you for new discounts. Got married? Had a student make the honor roll? These updates matter.

4. Review and Adjust Your Coverage as Your Vehicle Ages

Your auto insurance needs change as your vehicle gets older and decreases in value.

When to Drop Comprehensive and Collision Coverage

Comprehensive coverage

pays for damage to your car from non-collision events (theft, vandalism, weather, hitting an animal).

Collision coverage

pays for damage when you hit another vehicle or object.

Both coverages are optional once your car is paid off. As your vehicle ages and depreciates, paying for these coverages may not make financial sense.

A general rule: if your vehicle is worth less than 10 times your annual premium for comprehensive and collision coverage, consider dropping these coverages.

A Temple driver with a 12-year-old truck worth $3,000 was paying $600 per year for comprehensive and collision coverage. When he dropped these coverages and kept liability protection, his premium dropped by half.

Before dropping coverage, consider:

- Could you afford to replace your vehicle out of pocket if it were totaled?

- What's your vehicle actually worth? (Check Kelley Blue Book or similar resources)

- How much are you paying for comprehensive and collision?

Keep in mind that liability coverage is required in Texas and should never be reduced below state minimums (though higher limits are recommended for better protection).

Reassess Your Coverage Limits

On the other hand, if your financial situation has improved, you might want to increase your liability limits. Protecting your assets with appropriate coverage is just as important as saving money on premiums.

This is where working with an independent agency helps. At Winkler Insurance Agency, we can help you find the right balance between adequate protection and affordable rates.

5. Improve Your Credit Score

In Texas and most other states, your credit score significantly impacts your auto insurance premium.

Why Credit Matters for Insurance

Insurance companies use credit-based insurance scores

to predict the likelihood that you'll file a claim. Studies show a correlation between credit responsibility and claims frequency, so people with higher credit scores typically pay lower premiums.

A poor credit score could increase your auto insurance premium by 50% or more compared to someone with excellent credit—even if you have identical driving records.

How to Improve Your Credit for Better Insurance Rates

Pay bills on time:

Payment history is the most important factor in your credit score.

Reduce credit card balances:

Keep your credit utilization below 30% of your available credit.

Don't close old credit accounts:

Length of credit history helps your score.

Check your credit report for errors:

Dispute any inaccuracies that could be dragging down your score.

Be patient:

Credit improvement takes time, but even small increases can lower your insurance premium.

Improving your credit score benefits you far beyond insurance rates. It affects loan interest rates, housing options, and sometimes even employment opportunities.

Bonus Strategy: Shop Around and Compare Quotes

Insurance rates vary dramatically between companies. One carrier might consider you high-risk while another sees you as a preferred customer.

This is where working with an independent insurance agency provides real value. Instead of getting a quote from just one company, you can compare rates from multiple carriers at once.

The agents at Winkler Insurance Agency in Temple, TX work with several insurance companies, allowing them to find you competitive rates without requiring you to spend hours requesting quotes yourself. They compare coverage options side by side, ensuring you're getting the best protection at the most affordable price.

Making Your Auto Insurance Work for You

Lowering your auto insurance premium doesn't require sacrificing the protection you need. With these five strategies, you can reduce your costs while maintaining coverage that protects you, your family, and your assets.

Small changes add up. Bundling your policies, adjusting your deductibles, claiming available discounts, reassessing your coverage, and improving your credit can collectively save you hundreds of dollars per year.

Ready to see how much you could save on auto insurance? Contact Winkler Insurance Agency in Temple, TX for a personalized quote. We'll help you identify discounts you qualify for and find coverage that fits both your needs and your budget. Get your auto insurance quote

today.